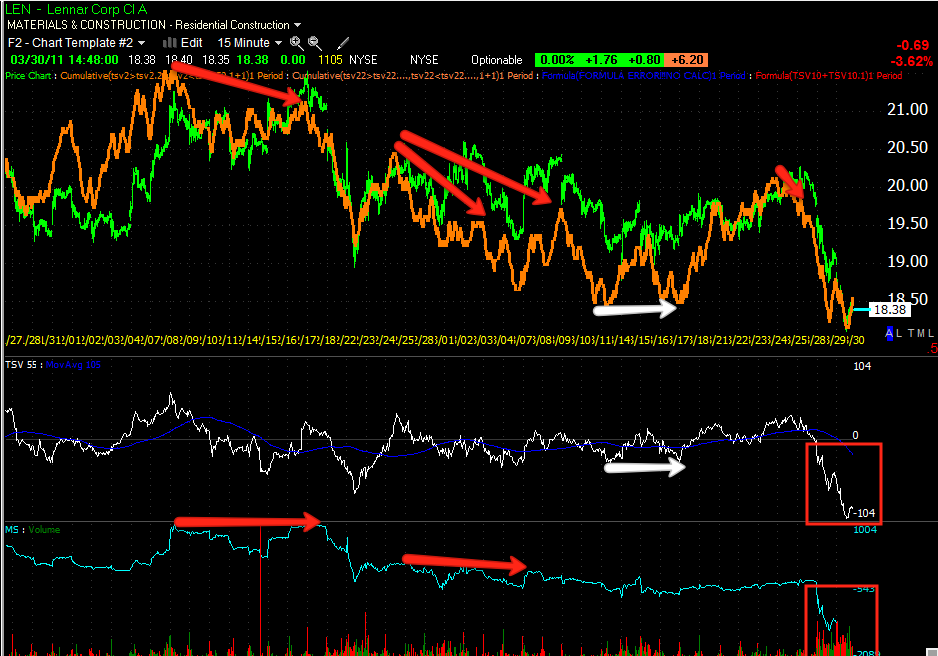

The trades that are the most obvious send people all to one side of the boat and eventually it capsizes.

Here's a great example...

For historical purposes, I'm using the Dow Jones Oil and Gas Index. So here we have a 300% gain and one of those bubbles that was like all others, "different this time". Whether it be peak oil, corporate control over the administration, or any number of reasons, there was no end in site of what oil would do, right up until the end, which by the way, 3C nailed the reversal in USO within 1 week; considering there were about 280 weeks to the trend, that's pretty impressive. The posts are on Trade Guild. USO lost about 80%, for commodity traders operating on sometimes lofty margins, this was a disaster and put many young and upcoming commodity traders in the unfortunate position of being the guy who took down the hedge fund. I recall that week very clearly, Cramer was on Mad Money telling people that they needed to be contrarians and the next bad weekly oil inventories report that came out, they should be buyers. I remember this so clearly because it's probably 1 of maybe 20 times I've watched Cramer and I remember seeing the signals suggesting the reversal was coming and finally I thought it was incredibly laughable that millions of viewers all doing the same thing was "Contrarian". In any case, those that did what Cramer said were left holding the bag. Being the trend was so long, I would dare to say that many thought it was a blip and would recover, but it didn't and I know of several traders I knew at the time who just wouldn't let go of their longs.

Today a similar situation appears to be playing out...

By now, it's very clear that extraordinarily accomodative monetary policy has been behind the move up in the market since March of 20009. Just look at how the volume faded into the uptrend and exploded into the lateral trend.

Here's a rough timeline for Fed easing that levitated the market. Unemployment at the bottom at March 2009 is 8.6%; unemployment is one of the reasons for QE. Today unemployment is higher then at the market lows. QE has failed to do anything but levitate the market, meanwhile insiders have been selling consistently since April of 2010. The argument of why this time is different is the many experts who insist that the Fed must continue with QE and will enter round 3 in 2011. This week we've seen several events from Fed speakers hawkish tone to the Fed experimenting with reverse repos/draining liquidity from the markets (the opposite of QE).

Here's the S&P 500 in green and the CRB (commodities index) in white, nearly perfect correlation. Through QE, the Fed has flooded the market with cheap money under the guise of kick starting lending, but banks have different ideas about it. They take the cheap money at nearly zero interest rates and invest in risk assets: equities, precious metals, commodities.

As we have seen, a trend in inflation has emerged throughout various manufacturing reports.

A week or so ago, MIT projected 2011 inflation will reach 8%

Manufacturers and a number of different corporations are feeling the squeeze in margins with higher input costs, the effect...

NKE passes costs on to consumers and loses 9% in one day.

RIM experiences a similar margin squeeze...

and drops over 11% in one day.

It seems the Fed is now taking real inflation seriously. Looking at this week's Reverse Repos and the hawkish tone from regional Fed presidents, it seems the Fed is letting on that rates may rise soon. The damage is probably done to most equities, but if something isn't done, the damage will be a lot worse.

Remember it was a sole individual in Tunisia that started the entire MENA crisis as standards of living and inflation costs hit people across the world. China is another example, I won't go into depth, but they've hiked reserve requirement ratios for banks at least 3 times this year in an effort to drain liquidity and cheap, speculative money that has given rise to inflation in equities and commodities.

So is there a shift coming in commodity prices? We're very early in the process of assessing this possibility, but it could be a rewarding trend.

Above is a "corn" fund. First of all check out the volume rising as prices rise, this is the hallmark of a healthy trend. However recently on this weekly chart, volume has gone red and we have a bear flag type pattern breaking the uptrend.

On a daily chart, the red volume uptick can be seen as the uptrend goes lateral and then makes a lower low.

CORN on a 30 min 3C chart shows several distribution/reversal points.

Now, here's the difference n commodity indices and where you want to be and where you don't. In red we have the most commonly used gauge of commodity price action, the CRB index. In red we have the Continuous Commodity Index ETF. Note the correlation between the two until this week as they diverge. Why did they diverge and what makes the Continuous Commodity Index a better way to gauge commodity inflation? The CRB is weighted differently and has substantial weighting in energy. I expect the trend in energy will continue to rise. The CCI has equal weight to each component and isn't distorted by energy, making it a better index to gauge commodity inflation.

I'm not saying to short the CCI, but there are unique equities that represent different commodities and some of those will have potential for being good short trades if this very early trend change is real and depending on central banks, especially the Fed's actions.

The notion of "this time it's different" may be in the midst of being proved wrong right now as it has been for hundreds of years in dozens of bubbles. So I'm starting another watchlist of various commodity producing and related equities. As I said, this is very early on in a possible trend change, but as you saw with oil in 2008, markets fall a lot faster the they rise and there may be a very significant opportunity in this possibly emerging change of trend.

| Theme by Thur

| Theme by Thur