As for the usual averages...The story is the same among all of them with slight differences.

SPY 2 min relative positive...

I suppose the Futures overnight will give us our first clue as to whether these averages see more building or not, but I would think with some positives in place, as minor as they may be, futures should hold on at least until the open (in underlying trade).

With the I-Phone 5 coming out Wednesday, we have some interesting information today on the back of a -2.63% drop in AAPL and another -.40% in after hours trade putting AAPL at $660 ($3-$5 away from some stop congregation levels). We learned today that in a poll conducted, 88% of Americans said they can't afford AAPL products and another 51% relied on credit to purchase an AAPL device.

Later in the day we learned that revolving Consumer Credit is on the decline with the largest sequential (2 month) drop since Q1 2009. Whether this has anything to do with AAPL's performance today, I have no idea and I don't really care, but it is curious.

As mentioned earlier today, I've been waiting for AAPL $680 to fill out the newest Put position which was completed on 9/4. The September portion of the position is close to breaking even, the October portion is up 17% today as AAPL closed red for the month today.

A weak relative positive divergence on the AAPL 5 min chart can be just seen, beyond that, damage.

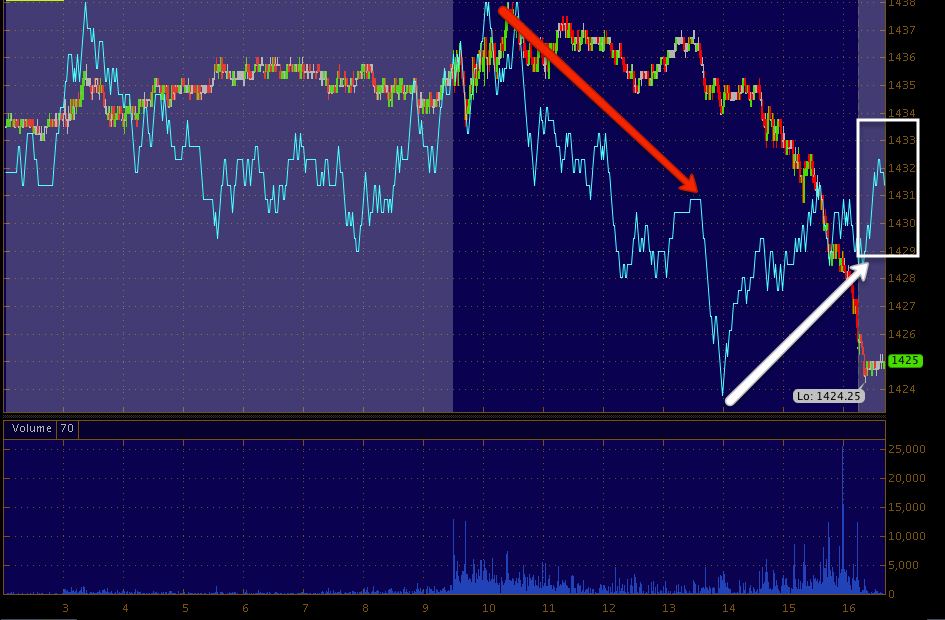

So the bottom line is how do the Futures 3C trade (not price) hold up overnight? Do they build of just maintain position?

In either case, major damage was done today to an already large divergence and period of heavy distribution.

Curiously equities underperformed just about every asset class out there, they have also been the most extreme in their moves higher. It seems that the best case scenario was priced in already and is being re-priced, but that is not the way we have found the market to work. More typical is the moves needed to get buyers to step in and create demand are sold in to by smart money and that appears to be exactly the case here as we can see divergences worsen right at specific breakout levels.

I find it strange that there are macro-fundamental events that "could" have a big effect on the market coming as soon as Wednesday, yet risk is apparently off the table well in advance of that, when normally a holding pattern would be more appropriate. I can't help but wonder if smart money is a bit smarter or better informed that the law would provide for.

As for some other positions performing well, UNG, our 1 favorite long position acted well today in the face of a melt down, up over 5%, but we expected UNG to strengthen this week.

I can not due the ECB issue justice in this piece alone, but first lets review what the ECB did and did not do. They did not adjust rates, they were left unchanged. The SMP bond buying program is effectively dead, replaced by the new bond buying program which is drastically different, here are some of the highlights (keep in mind that the German Constitutional Court's ruling this week could significantly impact the ECB bond buying and could make conditions attached to it different than originally intended -even though we have few details on those conditions).

-The ECB will purchase sovereign debt in the secondary market (much like the F_E_D, the ECB is forbidden from participating in initial auctions).

-The ECB will buy debt only up to a maturity of 3 years (when EU countries have sought bailouts because rates were prohibitive, effectively locking them out of debt markets, it has always been the 10 year bond that has been the benchmark-what the ECB thinks they will accomplish with 3 year debt that is beyond me).

-The ECB will HOLD the debt until maturity with specific caveats. This is where Germany has a major disagreement as the ECB's charter prohibits the financing of a sovereign nation.

-After buying any debt in the up to 3 year space, the ECB will sterilize the purchase, meaning they will sell an equivalent amount of bonds/securities so no new money is put in to the financial system which is supposed to contain inflationary pressures from non-sterilized buying-essentially what QE was)

-The ECB will NOT buy any debt (no matter how out of control the yields become) unless the issuing country first requests the ECB buy.

-Any country requesting ECB assistance in buying their debt to hold down yields will have to submit to a memorandum of understanding and meet certain fiscal/financial conditions or otherwise known as an adjustment program

-The ECB will now accept any collateral pledged for credit lines with no minimum credit rating (all of the decent collateral has already been submitted in LTRO 1 and 2 so there is little decent collateral left).

Initial problems I see:

The 3 year space is essentially worthless, these countries need cheap credit for 10 years to give them time to right their fiscal house. Whenever default of a PIIGS country is discussed, it's always revolving around 10 year rates, I've never heard any distress over 1-3 year rates. Secondly, Spain which is the domino that the EU cannot afford to fail, has already made clear they WILL NOT accept any assistance tied to fiscal adjustment programs, therefore it becomes very difficult and much more unlikely that sovereigns will tap this ECB program as once they do, they have essentially given away the last shred of sovereignty and politically that is suicide as G-Pap in Greece found out and as Greek parties like Syriza and now even the Neo-Nazi party in Greece have learned as they are seeing a huge swell in support as they oppose the Troika striping them of their sovereignty with the most recent example coming last week in which the Troika demanded Greece make labor reforms including a 6 day work week and effectively disbanding the labor unions which are culturally embedded in Europe far greater than Michigan or Chicago ever dreamed.

The 3 year language is especially interesting as it sounds like the 3 year banking LTRO program, perhaps the ECB will sacrifice the LTRO and let banking problems run the course they have run in Spain, let them become sovereign problems and then deal with the sovereign. LTRO was a huge failure as it did nothing that the ECB envisioned.

The details regarding the fiscal adjustment countries MUST submit to are unclear, Germany will almost certainly require a standard so high that no one uses the program. Furthermore, if after the ECB buys the bonds the country does not stick to the fiscal adjustment program, the ECB will sell the bonds, a sort of punitive clause.

Argentina tried a similar tactic including sterilizing purchases, like many in Germany have warned, the ECB's program will cause inflation. In the case of Argentina, it caused hyper-inflation.

Today we saw sovereign debt yields rise for the first time since Draghi announced the program last eek (initial knee jerk reaction was lower yields), bond traders are smart cookies and know something doesn't smell right here. This could all be a moot point of Germany shoots this down as unconstitutional as the ECB is made up of each Euro-zone country's central bank and the only one with any real cash to put out there is the German Central bank, affectionally nicknamed, "BUBA". I'm not quite sure why Draghi has put himself on a collision course with Merkel other than the fact that the ECB is virtually a puppet of Goldman Sachs who was the one in fact to leak to Bloomberg the day before the ECB announced its decision, EXACTLY what the ECB program would look like, most likely because Goldman designed it. Remember where Draghi comes from... YES, he comes from Goldman Sachs.

Also don't forget why the Euro-zone exists, many think it was US-envy, in fact it exists for one reason only, so the manufacturing juggernaut that is Germany has a completely free trade zone in which to export their goods, this is why countries have to meet minimum standards before being accepted (they have to have a stable economy that makes their entrance in to the Euro worthwhile to German exports).

Once Germany sees no hope of the EU facilitating exports or it becomes clear that the costs outweigh the benefits, say goodbye to Germany and if the EU puts enough financial drain and contagion exposure on Germany, the politicians will leave the Euro zone long before they are kicked out of office.

Why do you think Germany is so willing to let Greece leave or kick them out of the EZ? They serve no purpose in German exports.