As mentioned earlier, ES quickly retreated BELOW its VWAP starting around 3 p.m. and really picking up pace minutes before the close, by 4:30 ES was trading at 1374.25 which is only about 1 point off the intraday lows after having reached 1382.75. Think about that, ES gained 8.5 points and then lost all but 1 point in the last hour of the day.

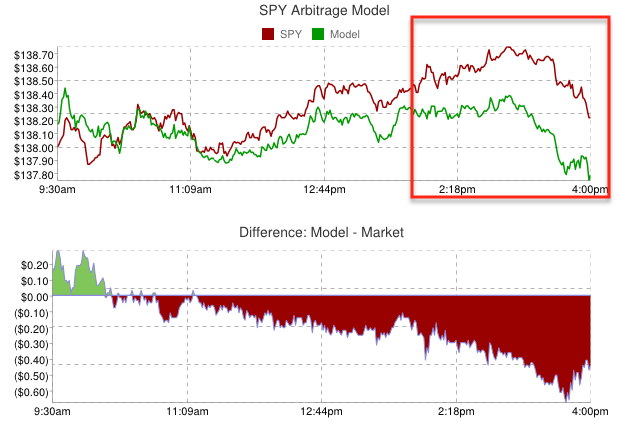

ES actually moved below the CONTEXT model and quite sharply as you can see to the far right.

Some other important averages and their 50-day moving averages...

You might expect with a little intraday bounce to see yields rise and bonds fall, not the case...

As far as the sector that carried the day, it was Tech as you might imagine, but remember what the Q's and AAPL looked like on 3C today (and when I say Tech, I pretty much mean AAPL).

The 3 main risk groups broke down like this: XLF -1.48 , XLK -.66, XLE -1.26.

HYG (High Yield Corp. Credit) broke below its 100 day moving averge today for the first time since November.

The move in the $AUD was definitely interesting (see last post), but the retreat in ES and the market in general can't really be attributed to dollar strength.

For those in to Dow Theory or Dr. Copper, the divergence between both and the Dow-30 is obvious, but this is what I've been showing you in the underlying trade for some time so it's not surprising, it is however a red flag.

I've been saying (generally speaking) I wouldn't be long anything in this market right now, the worm can turn too quickly to get out of the way. So much for Goldman's long the Russell 2000 call discussed last night.

As of today's close, up to 43 days of R2K longs are now at a loss, that's nearly 2 trading months (22 days per month)

In any case, something odd seems to have went down today, maybe Bernie' speech will shed some light or perhaps this is just the continuing change of character.

The dominant P/V relationship in the major averages was Price Down/ Volume Down which only tells us the market is not in an oversold position, although that is to be expected on today's light volume.

Today's movement came from lower than avg. volume (NYSE 725 mln, vs. 805 mln avg; Nasdaq 1330 mln, vs. 1699 mln avg),

Decliners outpaced advancers (NYSE 640/2387 Nasdaq 466/2079), and for the first time I can remember in a long time, new lows outpaced new highs (NYSE new highs/new lows 23/59 and NASDAQ new highs/new lows 28/72).

The A/D ratio however is enough to create a 1 day oversold condition, that is unless we are t the edge of the cliff and then 1-day oversold conditions won't matter.

I have a feeling something is going to hit the wires soon, maybe from Bernie' speech, maybe on the EU open, but today's market action just didn't feel right toward the end of day, or in other words, something is changing. You know where I have stood on this market and a snap wouldn't surprise me, when the snap comes is often a surprise.

The last month and a half or so have seen the underlying trade deteriorate badly, not only in 3C, but breadth, margin, flow of funds, insider selling, credit markets, carry trade unwinds and now the re-emergence of EU problems and that apparent problems in the US and China as well.

I'll probably update again after Bernie speaks or if anything unusual happens in ES or currencies.