The early chatter is the Swiss National Bank is or will adjust the EUR/CHF peg as the Euro was approaching the $1.32 level (side note: the last Goldman Sachs "Buy the Euro" note of 10 days ago was stopped out with their customers taking a substantial loss, I believe their call was buy to $1.40!)

The Euro (EUR/USD) almost breaking the important $1.32 level with a low this morning of $1.3211 and Goldman's stop at $1.34. Of course while Goldman clients lost, the GS trading desk likely took the other side of those trades and made out. As another aside, GS has announced they are giving up on EU calls due to the volatility and unpredictability in the EU. Unpredictability? Everything is going down, why would they issue a long EUR call? That's a rhetorical question.

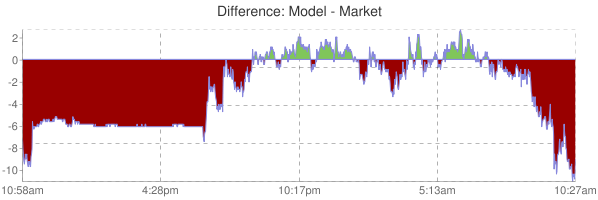

The Broad risk basket according to my new indicators looks like this, which seems to simply be a legacy arbitrage Euro/FX trade.

The commodities basket vs the S&P is higher this morning, however it is not higher over the last day as the S&P has broken above the 11/23 highs (white trendline) while the commodity basket is still below the 11/23 highs, so briefly put, commodities are doing what they are supposed to do when the dollar weakness, however ES/S&P 500 is a bit more excited then the typical risk assets that rally with it.

Here again the correlation between the Euro and the S&P is a bit off, while both are moving in the same direction as they should, the S&P is a bit more excited.

Part of this may be explained by the Euro losing ground over the US holiday and the S&P just hasn't been marked to the Euro, one easy way to find out is to count how many pips the Euro moved since the 4 p.m. 11/23 close and see what the difference is in Dow points; 1 pip in the EUR should equal 2 Dow-30 points, I suspect that correlation is a bit higher this morning, but I will make the count after this post.

Early momentum in Financials is clearly leading the S&P on an intraday basis.

On a longer term basis, and this was also an easy way to identify the top and one of the reasons I told you to short the S&P on that Friday I wasn't feeling well (11/11) , Financials are leading the market much lower. That 11/11 trade as a straight S&P trade even with today's early bump was worth 7.20% and using SPXU as I have been recommending, well over 23%.

Interestingly, because High Yield isn't correlated to the EUR, it is moving down this a.m., so while equities are risk on, High Yield Credit is leaking lower and as we know, credit leads stocks.

After Wednesday's sell-off in High Yield Corporates, it is just about in line with the S&P this morning.

Rates also sold off on Wednesday and the market tends to revert to rates, there's a fairly decent correlation this a.m., but just recently in the red box rates are starting to diverge from equities.

On a long term scale, rates predicted the top as well as 3C both in July and in November and there's still substantial downside before equities revert to rates, assuming rates don't move lower.

I just loaded the SF 3C template and will update that next.