With a post like this, I'd almost need a publisher to put everything in place so hang in there with me.

First for those who may have head the phrase, but were too embarrassed to ask (Ask away, if I can help I will), this is the definition of a "Carry Trade"

OK, now you have the basic idea, popular carry trades center on borrowing the Japanese Yen and typically buying the AUD (Australian Dollar as they have a pretty decent interest rate), the Euro or the USD. You may recall about 4-5 months ago I was tracking these carry trades very closely almost every day using some white currency charts, as the market started to get toppy and volatile we saw nearly all of them shut down. The carry trades started in earnest early November 2012 just before the November 16th market bottom that came as a result of the 7-8% pullback after QE3 was announced on September 13th.

Who, Why, When and How?

A lot of carry trades are used by institutional investors and especially Hedge Funds. Hedge Funds have what's called "AUM" or Assets Under Management, a hedge fund can increase their effective buying power or create leverage by engaging in a carry trade, but unlike the typical explanation of "Carry" where the trader is trying to capture the differential in interest rates, hedge funds are using massive leverage on these trades of 10 to 1, 100 to 1 even 200 to 1, which increases their buying power/leverage; that's the who and why (at least one version). Typically they engage in these trades when they are pretty sure things like interest rates are stable, when the F_E_D was giving express calendar dates for when QE would start and stop and when the earliest time they might consider raising rates, this made for a more stable environment in which the traders could count on things staying relatively the same. Imagine a 300 pip move like last night and say you're making/losing $10 a pip at 10x leverage that's a $30,0000 loss on 1 contract, now imagine how many contracts they have open and/or a higher leverage multiple. They can do really well or they can lose their shirt in minutes so a stable environment is important. Finally the "How", would you be surprised to hear that most of these hedge funds are not content making 3% or so (even leveraged) and typically use the proceeds to invest in equities and other risk assets hoping to make a larger return, for hedge funds that leverage is the primary allure to the carry trade and it typically goes in the market.

What does this mean to us?

On Tuesday (July 9th) in the "Daily Wrap" I said the following...

"The open and close of the last two days is virtually unchanged as you can see above on the candlestick charts, meaning almost all of the gains came from overnight futures trade....I identified the currency cross that was driving overnight markets earlier at the open, it was the AUD/JPY, but if you superimpose the pair over ES you can see the two never really separated the entire day. I can post a bunch of charts, but it really doesn't matter much, however after looking at the individual $AUD and JPY charts, it looks fairly clear that the $AUD is going to come down in the near term and the Yen rise which does in that pair"

The earlier "Pre-Market" post from Tuesday morning that I was referencing can be found at the link with the charts that showed why I thought the Carry Pair would be moving down. This is an excerpt from that pre-market post Tuesday morning...

"As far as FX carry trades, nothing looks very interesting except the AUD/JPY, but it looks like it's losing some steam, if it does as I suspect it will, we'll see what that does for the market after a pretty nice overnight session."

The main point is the pullback I first identified was directly responsible for yesterday's market gains of 0.02% in the S&P-500, the overnight ramp led by the carry pair wasn't there to gap the market up and as we had already seen the previous days, the market had very little strength during regular hours as evidenced by the closing candles which were dojis and stars (meaning the open and close were almost identical), in fact I posted this chart and comments to make the point in Tuesday night's "Daily Wrap"

I don't remember which post, but some time yesterday I mentioned that the observation I had made pre-market the day before (Tuesday, July 9th) about the AUD and Yen 3C charts looking like the AUD/JPY pair was going to come down which it did and continued overnight so Wednesday the FX pair couldn't drive the market higher overnight (because that's where all the gains were occurring-on the gap in the a.m.), that left the market flat yesterday until the Berni...

The point thus far is that beyond the negative divergences, leading indicators and anything else, there was only the overnight carry ramp to drive the markets higher. In fact yesterday's nearly flat close needed a lot of help just to do that, remember yesterday's SPX arbitrage being used to hold the market from falling apart?

Last night in, "Now That AH is Closed" I posted this CONTEXT ES model chart with the following comment...

It turns out I was right and sort of wrong, CONTEXT above from last night at -30 ES points was reset this morning, take a look at the new chart below...

Here they are talking about the AUD/JPY Carry that has been driving the market in overnight gains being dead this morning...

"Another day, another 3-sigma swing in one of the biggest and most important FX carry-trades. AUDJPY is collapsing this morning as the smell of leveraged trades being tapped on the shoulder is all too fresh...."

Here they correctly identify the type of market conditions that are ripe for carry, "Low-volatility" and as we'll see, they say they were starting a large carry position again recently which we will see from my earlier posts is correct.

"Critically, carry trades are predicated on leveraging low returns in a low-volatility world; the shocks from a few weeks ago saw carry unwinds en masse - but all it took was a handful of Fed officials and Draghi/Carney's chatter and they are backing up the truck of the carry-express once again "

This part they either got incorrect as we identified the start of the decline in the carry trade early Tuesday morning OR... the market knew about it. You may recall in my post on the subject today before I had read this I said,

" Something changed in the AUD/JPY and fast, I didn't read the article from earlier, but from the looks of 3C, I'd say something like a carry trade being closed quickly was what happened here."

"On a 2 hour chart where trends are visible without noise/details, the accumulation is clear, but so is the very sudden change in character as the most recent divergence is very sharp, very strong.

It does look like the AUD/JPY pair was closed out, I still haven't read that article, but perhaps something there makes sense with the above."

In fact, other than this post, the earlier post, "Strategic Update" which those comments came from today may have been the most important post all week, it's not long, I strongly suggest just taking a look at the charts again, the "Backing up the truck" or large positive divergence is very evident as it the very fast negative change.

OK, now the premise is pretty much laid out, lets look at the facts.

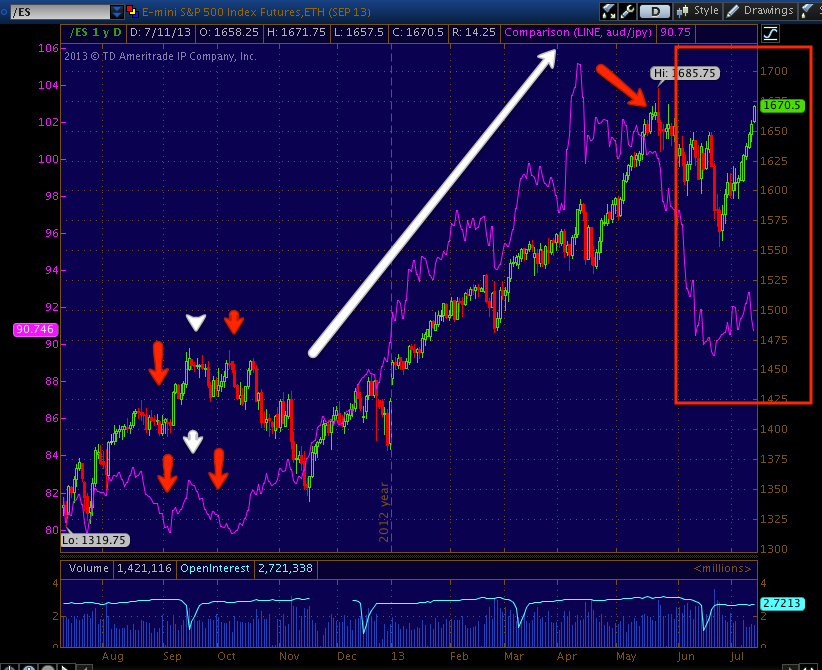

The charts below are of ES (S&P E-Mini Futures) in red and green candlesticks and the AUD/JPY "carry trade" in purple. There's no 3C on these charts, just a comparison between the price action between AUD/JPY and ES.

Right at November 16th, you can see the correlation move from lower prices in the carry that essentially means they sold assets to close the carry trade to the carry trades back on and the two moving in tandem together.

Note that around March the carry pair started to decline, this is about the time I suspected they were being closed out, you may remember I was following all 3 every day looking for changes in character that led to reversals in trend. To close a carry trade, the leveraged equity trades that were financed have to be closed, and the borrowed money (Yen) returned. The start of that process coincides with the market top and the trade is in what might be called a "Leading negative" position vs the SPX.

To give you proof of these trades being closed out, just think about the Market Breadth charts, other than what 3C is telling us, there must be other evidence of a mass migration out of stocks. Here's 1 example...

This is the SP-500 in red and a custom indicator in green, "Percentage of All NYSE Stocks Trading Above Their 40-day Moving Average". In any normal, healthy trend, higher prices should mean more stocks trading above their own 40-day moving averages.

This is the same AUD/JPY (purple) vs the SPX on a 4 hour chart so you can see how closely they are correlated.

This is the same 4 hour chart showing February to today.

Here's the post from earlier today, "Additional Charts" showing the Index Futures and 3C charts, just compare one or two of the charts of 3C (and Money Stream to give you two totally differently coded indicators and market averages) to what you see above.

This is a 60 min chart of the AUD/JPY vs. SPX futures (ES).

In somewhat similar fashion, here's a formerly perfectly in line (trend confirmation) 3C chart (30 mins) of Russell 2000 Futures suddenly plunging on a serious timeframe to a huge leading negative divergence, these charts formerly were all in line.

This is a 15 min AUD/JPY carry pair vs ES

The point here is to show in white the overnight ramp of the market by the carry pair leading to Monday and Tuesday's gaps up, but remember I identified a problem and said the pair would fall apart, thus in red the futures were not ramped via the AUD/JPY overnight and there was no gap up Wednesday and the market closed (SPX) at 0.02%.

Look at how badly the FX carry that has been supporting this market since November 16th, has fallen off; it reminds me of the 30 min 3C chart of TF above or this 3C ES 15 min chart from this morning's post linked above.

This is the FXA (AUD ETF) I showed earlier today vs the SPY, it's hard to get the scale correct here, but...

If I zoom in a bit, you can see how the market traded right with the AUD and thus the AUD/JPY.

The only disagreement I have with ZH's article is that they say the sudden panic to exit the carry trade (which means stocks would have to be distributed to close it, explaining why the 3C divergences are so sharp) was because of Bernie's comments last night, but as I've already clearly showed you with a linked post, Tuesday morning we were already seeing 3C distribution in the pair severe enough for me to say,

"As far as FX carry trades, nothing looks very interesting except the AUD/JPY, but it looks like it's losing some steam, if it does as I suspect it will, we'll see what that does for the market after a pretty nice overnight session."

So that may mean someone knew in advance what Bernie was going to say after hours the next day or there may have been another reason, either way, there was serious accumulation of the AUD/JPY as pointed out in linked posts above and it was suddenly and sharply distributed.

This leaves the market on a very precarious limb, not only distribution throughout and for some time, but sudden panic in the FX market up to 48 hours before Bernie ever spoke.