By now you are probably familiar with the importance I place on the Russell 2000's performance, it's not just me, but when Bern-ak-acide was before Congress, he cited the Russell 2000's performance in what he called the "QE Wealth Effect", the idea being that the market had risen and caused average Americans to gain in wealth, of course we know this to be a ridicolous arguement and certainly well beyond the F_E_D's dual mandate of inflation and maximum employment, levitating the stock market via a shell game that was Quantitative Easing, is certainly not one of their mandates and the ridicolous volatility QE on and/or off created an envirornment in which many Americans simply could no longer have faith in free, fair and open markets and as we know, they left the market by the billions ($).

In any case, the IWM/R2k was also the basis for my pre-Santa Claus rally period analysis. The bottom line was then, as now, the defensive Dow Jones Index led the market, while the broad Russell (a much larger sample size then the Dow and a much more diverse group of stocks) lagged. The end result? No Seasonal Santa Rally, despite very high expectations for one.

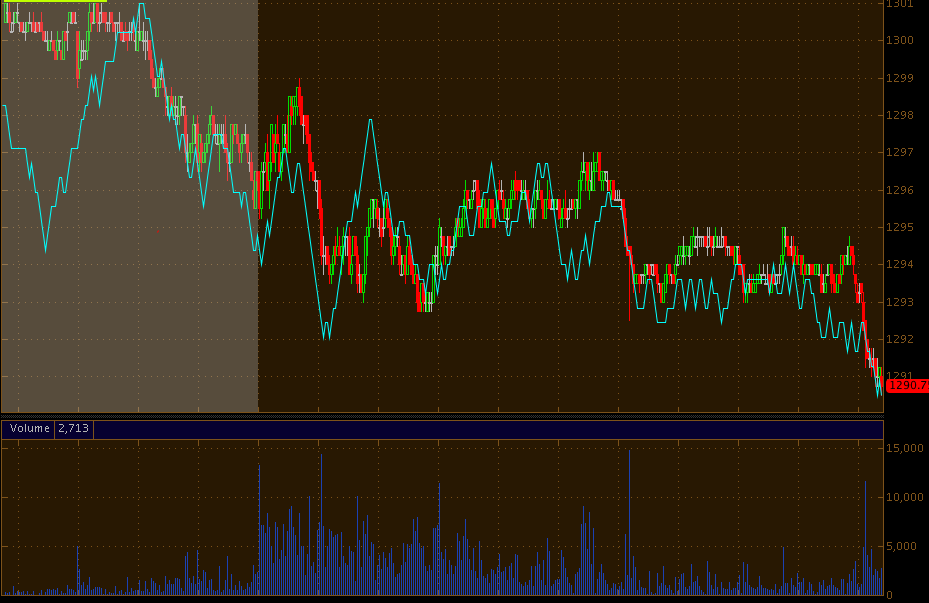

Looking at the market today, we see some green in the S&P, Dow and NASDAQ, although they did give up significant portions of their gains today. The Russell gave back all of its gains and then some to close red. On an intraday basis, from the IWM's high to the close, it gave back over 1.2% and it couldn't have happened in a worse place for the bulls.

Looking at the price pattern and volume, it's not hard to guess which way to the path of least resistance as the bearish wedge and the breakouts above the bearish wedge have all come on decreasing volume. In fact, considering today's gap up, even had the WM held onto its gains, the volume would make today very suspicious as volume hits a new low for the year. However, this new low in volume doesn't effect the bearish case, stocks need volume to rise in a healthy/ (Centrally) non-manipulated market, but stocks DO NOT need volume to confirm bearishness. It is said that stocks fall of their own weight, implying volume is not a major consideration, furthermore, lower volume is a distinguishing hallmark of a bear market.

If we look back to the last real bull market (void of manipulation by the F_E_D), we see what volume should look like.

Compare and contrast volume during the bull market starting in 2002/2003 vs the bull market starting in 2009 (while technically the 2009 market is considered a bull market by Dow Theory, I have a feeling when history looks back at this period, Dow Theory will have to be revised and the 2009 bull will likely be called "the biggest bear market rally ever" once we have a historical perspective).

I used a 200-day moving average on volume to illustrate the trend in volume compared to price.

As for the case for declining volume being a hallmark of bear markets, let's go back to the greatest bear in US market history.

Dow Crash of 1929 and subsequent bear market.

I think it is fair to look at the Financial sectors lost gains today as the sector was identified last week as coming out of rotation; while never attaining the same gains as the other 2 main industry groups, it did manage to climb in to the green and gave back 1.8% from highs to close.

XLF/Financials

Also noteworthy, if we average the gains of the 4 major averages, the Dow-30, SP-500, NASDAQ 100 and Russell 2000, we get an average gain of +.46%. Considering the gain, I find it interesting that the VIX was up 6.26% today (the VIX usually has an inverse relationship with the market).

The VIX is coming out of its own wedge, a bullish descending wedge. Low readings in the VIX imply complacency and as the VIX turns up toward fear, the market typically falls. The message of the VIX today was one of increased fear.

I'll have more for you in a bit, these are just some preliminary observations.