This weekend I had hoped to unwind, look at the market with a fresh pair of eyes and get a grip on the most likely near term outcome, I spent months (actually longer) making the case for the big picture outlook which is more bearish than I can accurately describe. The world economy and the market are in uncharted waters with no historical precedents to look to, I can only tell you that what I have seen over a long period of time has been as bad or worse than anything I've ever seen in the market and I've spent a lot of time studying historical markets including the 1929 market. There are simply no words because as we see with each passing week, the problems in the global financial web are beyond comprehension. I doubt there is anyone out there that can give an accurate forecast of just how bad this is likely to be, other than someone simply taking a wild guess as tens of thousands of pundits will, someone will be close.

Instead of having a relatively quiet weekend in terms of news flow, there have been a rash of events and stories that have simply muddied the waters even more. The main problem I see in analysis based on last week's readings is that (as expected) the fundamental events are becoming so unpredictable and at such a staggering pace, this seems to be one of the rare moments in which Wall Street is reacting rather than their typical planning ahead and setting up market runs and cycles. I intended to look very carefully for clues as to the near term movement of the market, instead I found myself more captivated by the fundamental events unfolding in Europe and what this means for the market big picture. As in the recent case of JPM, we see smart money is not always so smart. After discarding a lot of work in looking at near term charts after I saw the rather heavy news flow from Europe, I decided I'm going back to the basic, keep it simple, reduce the noise and look at the trends.

Speaking of JPM, Fitch downgraded JPM to A+/Watch

negative after JPM took a $2 bn. Dollar loss on a HEDGE position! The

$2bn loss is only the start, JPM will take larger losses as they try

to unwind the losing positions and in such an environment faces

additional downgrades as addressed by Fitch. Obviously the JPM news

weighed heavily on Financials Friday, but I still believe smart money

was aware of JPM's problems at least a month ago as I demonstrated

with the 15 min/1 day 3C chart, this was no small divergence or

ambiguous, this was a whopper, the kind I really like to see and

trade. As you will see later in this update, there was some surprising action in Financial momentum late Friday which leads me to wonder whether the weakness in Financials Friday was being used by Wall Street, especially if they already discounted JPM a month ago; this would allow them to pick up on some shares on the cheap for a near term move.

I found some late day evidence on a very short term 2 min chart that this may indeed have been the case as the positive divergence on the chart roughly correlated to the better relative momentum in Financials vs the SPX. I would expect to find such evidence on the short term charts, 1-2 minutes and I found it on both, here's the 2 min.

After the market's early upside momentum, there's a clear negative divergence which turned the market intraday, but there's a late day positive divergence that is just as clear. Remember PRICE IS DECEIVING and Wall Street (much like we try to do) often sells strength and buys weakness.

After the market's early upside momentum, there's a clear negative divergence which turned the market intraday, but there's a late day positive divergence that is just as clear. Remember PRICE IS DECEIVING and Wall Street (much like we try to do) often sells strength and buys weakness.

A Not so Surprising Surprise Out of China...

I found some late day evidence on a very short term 2 min chart that this may indeed have been the case as the positive divergence on the chart roughly correlated to the better relative momentum in Financials vs the SPX. I would expect to find such evidence on the short term charts, 1-2 minutes and I found it on both, here's the 2 min.

A Not so Surprising Surprise Out of China...

Saturday morning we got some no so

unexpected news as China's PBoC (People's Bank of China) cut

the Reserve Requirement Ratio for banks by 50 basis points, from 20.5% to 20.0%,

effective as of May 18. The move is expected to free up "an

estimated 400 billion yuan ($63.5 billion) for lending to head-off

the risk of a sudden slowdown in the world's second-largest economy"

as estimated by Reuters-it may be a little too little, too late for that. The move really wasn't a surprise as the

market has been discounting a RRR cut from the Chinese Central bank

on the back of consistent slowing economic data with some

moderation in inflation expectations which gave the PBoC a little wiggle room. Many feel the PBoC is behind

the curve with this rate cut (as is so often the case with Central Banks), as mentioned, the market has been

widely seen as already having discounted a RRR cut from the PBoC, so the impact it

has probably won't be as strong as if they had done this a month or

so ago, still it is easing. This is the 3rd

cut since last November, before that the PBoC had not adjusted the

RRR for 3 years; it's obvious China is feeling pain and pressure to

act. Ironically the cut in November came about 3 weeks after we

speculated there was major problem in China from our analysis of the

commodity markets. Analysts are still forecasting at least another

series of cuts that would be roughly twice the size of this weekend's cut by the end of the year as China struggles with manufacturing,

exports and a huge real estate market collapse, yet there remain pockets

of stubborn inflation and the move is still risky as inflation (which is measured differently in China than in the west, they actually account for the things we use every day like food and gas, whereas the West tends to view them as "Transitory"-a huge mistake in my opinion, especially at a time when these are huge expenditures for the average person).

It

wasn't too long ago that a soft landing in China was expected by analysts,

however these series of cuts (not to mention the commodities market)

all seem to indicate China may face a much harder landing than

analysts expect. With China's single largest export partner, the EU,

obviously falling apart at the seams, this is having a dramatic

effect on China as well as new investment there and other BRIC nations or emerging markets; which were considered to be the hope of the world just a little over a year ago. In my experience, when things turn south, it's very hard to get them turned back in a favorable direction and they take on a momentum of their own-just look at how much the EU has changed over the last year, going from trying to contain contagion to seeing actual contagion in the core-France's credit rating cut is a prime example.

Upon

the open of ES and the FX markets (EUR/USD) so far the cut, as

probably should be expected, has had little impact, perhaps no impact

with ES and the Euro both opening with a gap down tonight.

We

talked last week about the chance of a globally coordinated bout of

easing as we saw last November as the market was soft. We still

cannot rule out further Central Bank easing actions from the ECB,

which has now seen Germany (which has been fiercely opposed to any

easing as they still have a huge mass psychological fear of inflation

from the Weimar days) do an almost 180 degree turn in recent

statements that are much more dovish with a bias toward easing.

Greece. It's almost a dirty word in the markets now...

Greece

as I said last week is “Lehman x 1000” for the EU and is quite the concern for the Euro-zone as it should be, I mean in terms of survival of the Euro project. Germany last

week and many other EZ partners have been downplaying the risk of an

exit of Greece from the Euro-zone, saying things like, “It would

have been worse if it happened a year ago”, they've been saying this for months for a variety of different reasons, some to pressure Greece, more recently to calm the markets so the bond vigilantes don't attack the core. This is all for public and political (in Greece) consumption. The way Germany and others are portraying a

possible/probable Greek exit is to look at the money they have sunk

in to aid loans, Germany's share of money contributed to the failed

EFSF, their contributions to the ECB and IMF and that's about it, a very misleading perspective. As we all know, these

things snowball and are connected like a spider web in thousands of

ways in which one can hardly imagine. These losses of specific

contributions DO NOT take in to account the reality of the effect of

contagion as banks fail, likely every remaining Euro-Zone country

sees their sovereign credit rating slashed as Fitch warned it would

likely do in case of a Greek exit; this would push up yields on sovereign debt making contagion all the more real and likely to push

countries that are already teetering like Spain, Portugal and Italy right over the

edge with 10 year yields rising above any sustainable level of

interest, meaning they'd either all need to be bailed out again

(which the EU rescue funds cannot handle) or more likely more real sovereign

defaults. These slow motion train wrecks like the EU that we have

been watching over the last several years have a tendency to snowball

and gain momentum toward the end, we saw the same thing in the US

from the 2007-2008 period. There seems to be a critical point of no

return and the market smells it, then all heck breaks lose. In my

opinion, all of the ingredients are already in place, there's no more

uncertainty as to whether contagion can be avoided, the only

uncertainty in my mind is how long it takes the market to smell blood

in the water and for the point of no return to start to be rapidly

discounted in the market; we may in fact already be there.

It

must be understood that all of the EU bank loans (specifically German

ones) will be worthless with a Greek exit, then the EU banking sector

collapses and there simply isn't “Bazooka” big enough, real or

imagined, that can possibly deal with such a historic default. China

has already seen this in the cards and the once imagined "Savior of

Europe" has made clear last week they are abandoning bets in Europe

and looking to Africa for new opportunities; that's called, "Cutting your losses".

Just

Saturday the propaganda coming from the EU about “A Greek exit

won't be that bad” was shown to be exactly what it is, propaganda! Words are useless, only actions count and judging by Saturday's

announcement from the Troika (as Bloomberg reported), they full well know what kind of

trouble they are truly in.

Bloomberg

reported:

IMF,

EU, ECB Open to Changes in Greek Aid Deal, Real News Says

“The

so-called troika of the European Union, the International Monetary

Fund and the European Central Bank is

willing to make six important changes to Greece’s financial aid

agreement if a pro-European government is formed in the country, Real

News said.

The

Troika is willing to extend by one year to end 2015 the time for

Greece to cut its budget deficit as well as to proceed with a

restructuring of loans, the

Athens-based newspaper reported in its Sunday edition preleased

today, citing “well informed” sources at the European Commission.

The

Troika is also willing to maintain the force of collective labor

agreements, to alleviate the level of pension cuts or restore certain

pensions to previous levels and to keep wage levels in the private

sector and reduce the average tax burden on employees, the newspaper

said.”

If this is not just a typical EU sewing circle rumor, in

the near term, this is appears to be an obvious attempt to influence the likely new

round of elections that will come as a result of Greece being unable

to create a governing coalition which would be slated for mid-June. It is widely expected that the

anti-Troiaka parties that staged a stunning upset in last Sunday's

elections will win a second election hands down, which if you recall

the letter I posted from Syriza (the anti-Troika party that won

second place) would undo and turn over all former agreements

regarding the Troika bailout of Greece. Germany pushed too hard to

make an example of Greece and it backfired right in Merkel's face. There are so many ways in which it backfired that I would have to double the length of this post to cover them all.

It

remains to be seen if Germany will back this report by Bloomberg,

there's a lot of embarrassment for Merkel should this actually

happen, but it was Merkel trying to re-shape the EU with harsh,

heavy-handed measures that have caused the stunning reversal of

fortunes in which France has done a 180 degree about face and instead

of supporting austerity, is (going by Hollande's campaign pledges) going to go in the exact opposite direction that Sarkozy was supporting. Even in the end, Sarkozy pulled Merkel from the campaign trail as he saw she was dragging his numbers down in polls. The Franco-German

alliance has completely collapsed and become not just a setback, but

a force puling in the opposite direction, a conflict between the two countries that were allies in re-shaping the EU just several months ago. Whether the Troika rumor is

true, whether Germany truly would back it remains to be seen as

German news like Spiegel have continued this weekend to act as if a Greek exit is

still in the cards, still manageable and that Greece would still

qualify for aid as a Euro member (which is not the same as a

Euro-zone member using the Euro), however should Greece actually

defect from the EZ, feelings won't be so warm and fuzzy toward future

help as the ECB will sustain massive losses as will everyone else

involved in the Greek bailout except maybe the IMF as Greece will need some friends with money and it will likely find few in the EU. Then there's the collateral damage,

but for now, it seems it's more of the same from Germany in the

Spiegel article, “A Greek exit is manageable” don't be fooled-IT IS NOT! There's

a lot of uncertainty around this Bloomberg report and I suspect it

will cause a lot of volatility in the market this week as there are denials, confirmations, head scratching and everything else you can imagine.

"If" this is an accurate story, I

said in the near term the Troika willingness to restructure the Greek

deal is likely a political maneuver, in the long run if the

anti-Troika sentiment holds as it has been (actually increasing),

the Troika may find itself begging Greece to take the money to keep

them from leaving the Euro-zone and creating a tidal wave that will

effect every EU country and financial institutions around the world.

The thing about playing a game of chicken is there's always the risk

that one side will not blink and Greek citizens went to the polls

last Sunday and did not blink, Germany pushed them too far and they were a people with nothing to lose. Remember that Sunday, it may have been

the beginning of the end of the Euro-zone.

Speaking

of Sunday elections, as predicted here (which isn't much of a

prediction as it has been a trend), Merkel's CDU party suffered what is being called "a

surprising defeat" in regional elections at Germany's most populous

state North Rhein-Westphalia. It's not only the Greeks that are unhappy with Merkel, her missteps have put German tax payers on the hook in a situation in which they may take a TOTAL loss.

Karma?

Europe

caught a cold from the US housing bubble collapse and because of the

interconnected financial and global trade system, the US will absolutely

catch the same cold returning from Europe, except this time it will

be much worse than what the US passed on to the rest of the world in

2007-2008.

In light of this weekend's events, I've captured and thrown out a lot of charts. When things start to get this crazy, I tend to look for the larger trends that have less noise, in essence, I go back to the basics and try to keep it simple.

First lets just go back to the market trend basics from Friday's post... (Friday's Comments are below the first two charts from the post linked above).

"Lets just take a look a several months and what the market did, what traders expected and how the market made sure it wasn't as simple as it appeared. First we had 3 bounces that made higher highs/higher lows (I believe we called all 3 from bottom to top and back to bottom again near perfectly). Traders would take this as an uptrend, that is what it is (higher highs/higher lows), but we had additional information and used those moves higher to start short positions, then instead of the trend continuing up, the market saw a sharp decline and formed a bear flag. Now traders see a bear flag and expect the market to break down, the market did (in the yellow box), but it was a head fake, drawing in shorts on the break and then stopping them out as the market moved higher, we shorted here again. In the orange box there was strong upward momentum, that same day that it started we not only predicted what would happen, but 3C confirmed it and that strong, bullish momentum fell just as quickly as it went up. Since then we've been in decline and have formed another bear flag. Technical traders will view this as a bearish lag that will break down to start a new leg down, but as you can see over the past 4 major moves, Technical Analysis said one thing and the market did the opposite in the near term. If you don't believe traders see this bear flag and are shorting it, just look at yesterday's 2012 record NYSE short interest.

If we follow what we have known for a long time, the probabilities are for a solid bounce knocking those shorts out again, making the average trader wrong again. That's where the signals have been lining up, that's where the market trend probabilities are."

Now, tonight's charts... (Remember, I'm going to the basics and keeping it simple with medium timeframes that effect the near term, but have much less noise and more of a trend).

The 15 min SPY also has a positive divergence and a good overall record, calling the May 1 top and changing character as the flag formation developed.

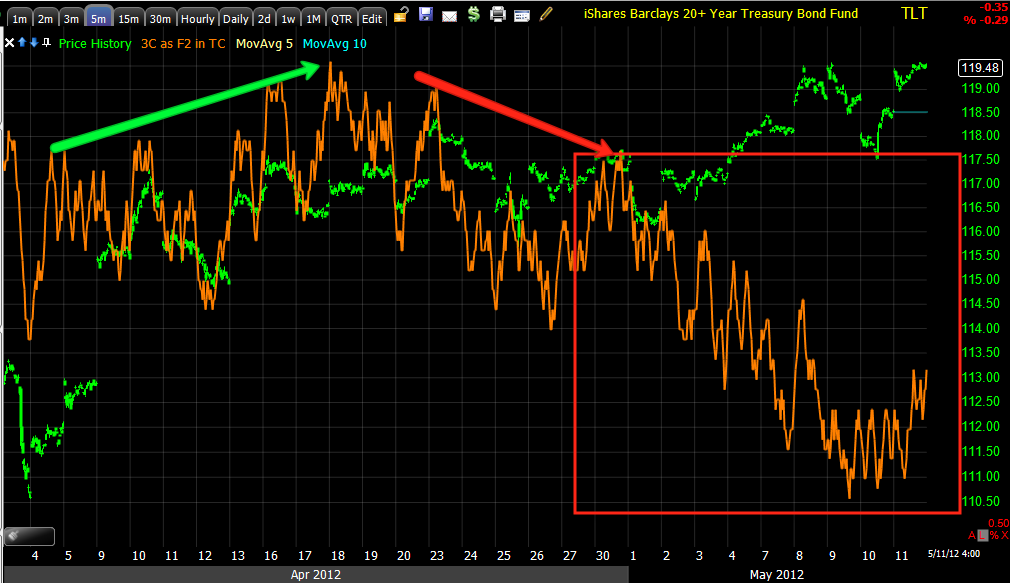

As for the TLT (Treasuries-Flight to safety trade) that was bothering me on Friday, I have applied the same, "Keep it simple" analysis and here are the same timeframe trends in TLT.

The 15 min chart that was also in line at the green arrow is showing a similar leading negative divergence. Remember, TLT or Treasuries are a flight to safety trade, the negative divergences in the TLT charts are in confirmation of the market average positive divergences above. All in all, that's pretty decent confirmation of the trends.

As for the near term Risk Asset layout, last Friday it had a few contradictory signals, the biggest was in rates, but "if" the 3C TLT chart is correct, that correlation should fall in line as Friday it was negatively divergent with the SPX, while credit was more positively correlated in the near term (what I mean by near term is the possibility of that one last bounce).

As of closing action on Friday, the Risk Assets looked like this...

Commodities underperforming-this is almost entirely due (in the near term) to the strength in the $USD over the last 10 days and weakness in the Euro. Longer term commodities are significantly negatively divergent, reflecting badly on the market big picture and China.

Although High Yield Corp. Credit did sell off at the end of the day, it still remains in a supportive position, that could certainly change quickly this week either way (more supportive or less), but as far as what we know now, it is still fairly supportive of the market and thus of a bounce.

One surprise in the late day trade on Friday was the financial sector that had been beaten up pretty badly by JPM's "surprise" (I'm being a little sarcastic given JPM's longer term charts showing it looked like smart money had known about this since at least early April) announcement. I found Financials showed BETTER relative momentum vs the SPX going in to the last hour and a half of trade. Any market bounce would need support from at least 2 of the three sectors I call the "3 Pillars"-Tech, Financials and Energy. Tech seems to look pretty decent just by looking at the QQQ 15 min chart, Financials showed better relative momentum, Energy would likely need a boost from the Euro and some weakness in the dollar to get back in to the game.

The Euro sold off a lot harder than the SPX correlation, meaning the SPX held up better than the legacy FX arbitrage correlation would suggest, this hints at market support, as I mentioned Friday, if the bears were solidly in control, the Friday afternoon sell-off on the failed test of resistance would have been a lot nastier to the downside than it was as the market's closed nearly unchanged and about exactly unchanged in the Tech heavy NASDAQ 100.

Perhaps the most encouraging (for a near term bounce) signal came from High Yield Credit, it held its ground through the close, it didn't sell off like the SPX did and hovered near the best levels of the day. Credit leads stocks, the larger picture in credit is quite ugly, but in the near term this was one of the more encouraging signals and more surprising ones.

As for the near term Risk Asset layout, last Friday it had a few contradictory signals, the biggest was in rates, but "if" the 3C TLT chart is correct, that correlation should fall in line as Friday it was negatively divergent with the SPX, while credit was more positively correlated in the near term (what I mean by near term is the possibility of that one last bounce).

As of closing action on Friday, the Risk Assets looked like this...

Commodities underperforming-this is almost entirely due (in the near term) to the strength in the $USD over the last 10 days and weakness in the Euro. Longer term commodities are significantly negatively divergent, reflecting badly on the market big picture and China.

Although High Yield Corp. Credit did sell off at the end of the day, it still remains in a supportive position, that could certainly change quickly this week either way (more supportive or less), but as far as what we know now, it is still fairly supportive of the market and thus of a bounce.

One surprise in the late day trade on Friday was the financial sector that had been beaten up pretty badly by JPM's "surprise" (I'm being a little sarcastic given JPM's longer term charts showing it looked like smart money had known about this since at least early April) announcement. I found Financials showed BETTER relative momentum vs the SPX going in to the last hour and a half of trade. Any market bounce would need support from at least 2 of the three sectors I call the "3 Pillars"-Tech, Financials and Energy. Tech seems to look pretty decent just by looking at the QQQ 15 min chart, Financials showed better relative momentum, Energy would likely need a boost from the Euro and some weakness in the dollar to get back in to the game.

The Euro sold off a lot harder than the SPX correlation, meaning the SPX held up better than the legacy FX arbitrage correlation would suggest, this hints at market support, as I mentioned Friday, if the bears were solidly in control, the Friday afternoon sell-off on the failed test of resistance would have been a lot nastier to the downside than it was as the market's closed nearly unchanged and about exactly unchanged in the Tech heavy NASDAQ 100.

Perhaps the most encouraging (for a near term bounce) signal came from High Yield Credit, it held its ground through the close, it didn't sell off like the SPX did and hovered near the best levels of the day. Credit leads stocks, the larger picture in credit is quite ugly, but in the near term this was one of the more encouraging signals and more surprising ones.

Taking these charts and Friday's analysis of the market's trends, the games it plays, etc., these charts fall in line with the opinions I posted in the post from Friday with the two charts linked above; despite my own personal feelings of the increasing unpredictability of the market's near term moves, I still can't ignore what the charts are showing as well as what we know about how Wall Street manipulates the market (the trend of Wall Street manipulation) and to me, they still show the highest probabilities are leaning pretty strongly toward that last head fake bounce I have been expecting.

We have options expiration week and with that comes volatility and perhaps a chance to really shake things up.

As far as economic data in the US this week...

As you can see, tomorrow is pretty much non-existient, it gets busier mid week.

As you can see, tomorrow is pretty much non-existient, it gets busier mid week.

I spent a lot of time looking at very short term charts, capturing them for this post and then completely discarding them as news events unfolded. I trust 3C, I trust the trends and the longer term charts more than the short term charts. I find that after looking at the market, my opinion hasn't changed much, I still feel the market is growing increasingly unpredictable as we have seen over the weekend and really in a huge way since last Sunday's Greek elections which totally reshaped the EU timeline, or as I would put it more bluntly, shortened the fuse.

I have NOT changed my big picture market view, I WILL NOT be closing short positions, but rather hoping and looking forward to a strong market bounce to add to them. All in all, I spent a lot of time this weekend to find my views haven't changed. To be clear, my views are not my personal opinion of the market, my personal opinion is I'm quite leary of some news coming out and Wall Street reacting rather than their usual planning in advance, but from an evidence based view, I have to say I still think the probabilities are with a market bounce. With increased amplitude and volatility it could certainly be a big one, especially with mass sentiment being so overwhelmingly bearish as we saw last week in the NYSE 2012 record short interest. I think those shorts are right, I also think Wall Street will see that there are so many traders leaning to one side of the boat that it would only make sense and benefit Wall Street to try to knock these shorts out of their trades. I will not be knocked out as the short positions we have been building are longer term based. I will use any strength in the market to add to those shorts and stand by the convictions I hold that are based on more than a year of analysis (this is nothing new for members who have been here during this time period-I'm no bearish "Jonny-come lately").

Have a great week ahead, with volatility I look forward to finding some quick trades this week to make some quick $$$, but I'm mainly focussed on where I think the larger opportunity lies.

We have options expiration week and with that comes volatility and perhaps a chance to really shake things up.

As far as economic data in the US this week...

I spent a lot of time looking at very short term charts, capturing them for this post and then completely discarding them as news events unfolded. I trust 3C, I trust the trends and the longer term charts more than the short term charts. I find that after looking at the market, my opinion hasn't changed much, I still feel the market is growing increasingly unpredictable as we have seen over the weekend and really in a huge way since last Sunday's Greek elections which totally reshaped the EU timeline, or as I would put it more bluntly, shortened the fuse.

I have NOT changed my big picture market view, I WILL NOT be closing short positions, but rather hoping and looking forward to a strong market bounce to add to them. All in all, I spent a lot of time this weekend to find my views haven't changed. To be clear, my views are not my personal opinion of the market, my personal opinion is I'm quite leary of some news coming out and Wall Street reacting rather than their usual planning in advance, but from an evidence based view, I have to say I still think the probabilities are with a market bounce. With increased amplitude and volatility it could certainly be a big one, especially with mass sentiment being so overwhelmingly bearish as we saw last week in the NYSE 2012 record short interest. I think those shorts are right, I also think Wall Street will see that there are so many traders leaning to one side of the boat that it would only make sense and benefit Wall Street to try to knock these shorts out of their trades. I will not be knocked out as the short positions we have been building are longer term based. I will use any strength in the market to add to those shorts and stand by the convictions I hold that are based on more than a year of analysis (this is nothing new for members who have been here during this time period-I'm no bearish "Jonny-come lately").

Have a great week ahead, with volatility I look forward to finding some quick trades this week to make some quick $$$, but I'm mainly focussed on where I think the larger opportunity lies.

No comments:

Post a Comment