Beware the F_E_D Knee-Jerk Reaction. Tomorrow is the F_O_M_C policy statement, for years there has been a trend of an initial knee-jerk reaction and it is almost ALWAYS wrong, usually being reversed within a few hours to a couple of days, it's just something I and others have noticed with such consistency that I ALWAYS warn before any major F_E_D / F_O_M_C event.

Sunday night I noted the volatility in the market last week when I was gone (almost all intraday) and I noted that ES (The S&P E-mini futures) was exactly where it was at Wednesday's 4 p.m. close as of the time of my writing late Sunday night, $1684. At 5:45 (now as I'm writing), guess where ES is? $1684.

For all the volatility and days that have passed, I find it odd that $1684 keeps coming up. If you put a daily VWAP on ES, it is currently at $1683.46. I'm not quite sure what to make of that, I doubt there's one super position being cashed out at a fill of $1684, it is likely more just a reflection of what stood out to me Sunday night after having been absent from the market for a couple of days, "no matter the volatility, the market is not moving much."

That brings up a couple of interesting charts, you've probably seen most of these (and keep in mind the VIX buy signal in our custom DeMark inspired indicator), but I figured they should be posted again as they really stand out to me, especially with this very recent range.

Remember the market breadth indicator I posted last night? The Percentage of all NYSE stocks above their 200 day moving average? I post these breadth indicators every once in a while in a major post, what struck me is as I updated my Telechart system after the close, I saw a note from Peter Worden which I almost never read and he had referenced the divergence between the NYSE and the same indicator I posted last night, I found that to be ironic, but both of us were looking at the same weakness in the market. I see those readings as proof the carry trades were closed earlier in the year and continued, he just noted the divergence.

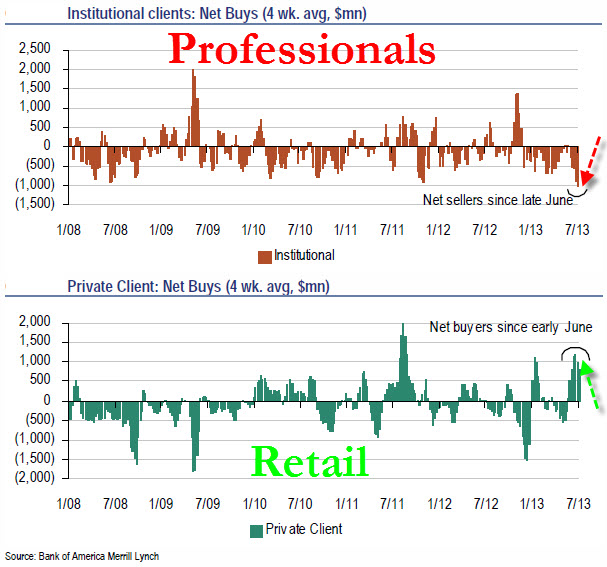

Something else I found interesting was a couple of charts that I don't have access to, here's one which is the case we've been making with retail sentiment updates vs. 3C charts....

This is the difference between Institutional positions and retail, institutional are net sellers as 3C depicts and retail are net buyers as sentiment indications depict. I also find it interesting that I identified November 16th (and the area just before) as the start of large carry trades as well as 3C accumulation for what I called the start of a "Cycle Up" and as we know from 3C, institutional money Sells in to price strength, they have to because of the size of their positions, take another look now at the last time Institutional money were net buyers and how the net selling has progressed.

This brings so many things to mind such as identifying the change in the F_E_D's tone as soon as they announced QE3 in September, as I wrote way back then, "It almost seems as if they are looking for an exit" and then everything they did since then moving closer to that direction until they finally said it, we had been making the argument 6 months before they actually hinted at it.

Also the difference between the charts above from May to July highs and how 3C can't differentiate between a sale and short sale as both come across the tape as sales. The collapse in credit earlier this year, the EXTREME dislocations in Leading Indicators, some of the largest 3C negative divergences I have seen going all the way back to the early 1900's, the Market Breadth Indications which are horrible and I could go on and on.

As for some SPY charts

*This is also about the area I expected a shorter downtrend to start and then be followed by the strongest up trend we had seen that would change sentiment which would precede "The Downtrend" we have been waiting for. Right around the 8th, everything changed and even signals showing the market was about to turn down were suddenly abandoned as if there was no time for it and the trend continued to the up trend we expected next. Even the size of the initial accumulation for the shorter up trend was right, it was way too small for the size of this one.

As far as tomorrow goes, the closing divergence in the SPY is clearly negative, this usually carries over to the next day, even over weekends.

I still find HYG's trade to be interesting and surprising to some degree.

First last night in this post I showed several charts that suggested we'd see early strength (gap up) in the market today, one of them was this 1 min positive divergence in HYG yesterday . Then today as the market started to lose its footing, it's a positive intraday divergence in HYG that turns HYG and the market intraday.

As far as other credit today, JUNK (High Yield) Credit usually trades almost indistinguishable from HYG, today Junk Credit continued to slide hitting new intraday lows for the last week or so.

Here's the second chart I don't have access to, but found VERY interesting.

As far as some other indications, commodities as a risk asset have not held up well recently.

As far as our Sentiment (Leading Indicators) go, FCT was worse today than yesterday, but still not horrible, except on a bigger picture basis which I also showed in last night's post. HIO is the same on a larger picture basis, intraday HIO was pretty close to in step with the SPX, however the market's bounce off the early afternoon lows saw HIO not participate in that move ending the day on a worse note.

There are quite a few assets I still want to look at and a lot of futures. I did want to show some of the positions from today as concepts, not individual trades, for instance last night I told you about MCP and what we'd be looking for including a move below the bear flag which should see an increase in volume and clear 3C accumulation, we saw the first two things, but not the 3C accumulation. MCP moved higher and at first it felt like, "I missed the trade", but we stuck to our discipline and were right for doing so as MCP closed down -1.4% so it is the concepts I want to highlight, not the good decision not to start a call position.

VXX was another, in this post I outlined exactly what I expected from VXX to open a long position/call position today including the following...

"the only thing holding me back right now would be looking for a head fake move below that triangle"

This is something we see 4 out of 5 times before a reversal, I jumped the gun a bit early, although I think the position will be fine as there WAS the accumulation on the head fake move that MCP did not have, but it is the concept that we follow that showed again to be the correct way to enter the position.

The trailing stops for URRE yesterday could have saved you quite a bit in profits today, but it is the re-entry in URRE long that I believe will come that is the concept I'd like to share with you.

I'll try to get these and more as well as other positions up for you, the concepts are the most important as they can serve you in just about any asset in just about any timeframe.

No comments:

Post a Comment