I explained last week how VWAP (Volume Weighted Average Price) is one of the few indicators that we know Wall Street uses and they use it to grade market makers on the NASDAQ and specialists on the NYSE proficiency in filling a large order for institutional money. Yes, Morgan Stanley (who also happens to be a market maker) is perfectly capable of placing orders, but there are many firms that place large orders and to get the best fill, they go to the expert in that stock, the market maker or specialist that represents that stock, these middlemen know the stock better than anyone, they now all the players, how those players react to different scenarios, etc, so when large orders go out, they are usually run through these middle men. If the market maker/specialist can fill the order at or at a better price than VWAP, they have done a good job and will get future business, if they give a bad average fill as measured by the VWAP, then they are not likely to get another chance at very lucrative orders that these people can make money off in a number of ways, including knowing what smart money is doing so they can tag along or heaven forbid, even do that illegal thing call "Front run" the order.

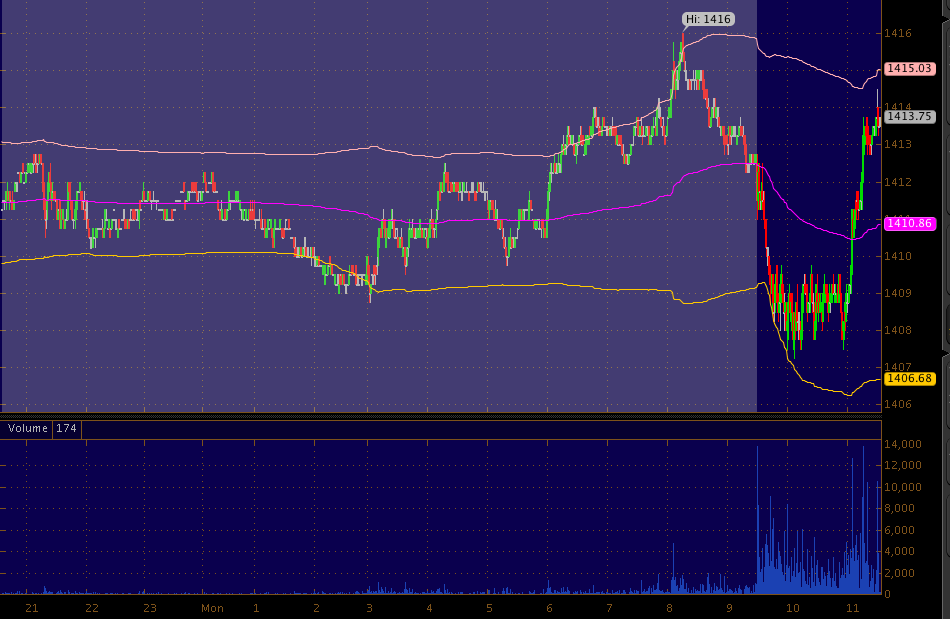

So looking at ES and VWAP this morning, there are no surprises here.

"If" I were a middle man in ES filling a short order, I'd be selling short at the pre-market highs at the 2nd upper standard deviation above VWAP, I'd have some clue that there's likely to be a correction or they may even have better information based on a number of sources and even order flow, I might trade a few contracts long at the lower 2nd standard deviation below VWAP, not only making a profit for my own account (market makers and specialists typically use to be responsible for about 30% of a stock's daily trading volume just from trading their own account), but would also put in a floor and support , it would show those watching order flow that some large orders came in and get ES moving up again. I'd then sell my contracts near the upper 2nd standard deviation for a nice personal profit and sell short some more ES for my institutional client and I'd be doing a fantastic job in their eyes filling them at 2 standard deviations above VWAP.

Remember, this crowd isn't trading in 100 lots like we are, they are moving on a massive scale, if they tried to execute an order that big all at once they'd drive the market way against their position, maybe even crash it before they had their position in place. There are High Frequency Traders that do nothing but "Ping for icebergs", meaning look for those large institutional orders, then when they find them, thy front run them and end up costing the institutions a lot of money on crappy fills as the HFTs drive price against them.

We can't afford to thin like the crowd on the StockTwits stream or Yahoo Finance message boards, we need to know how they think, but that's just to know how Wall Street will take advantage of them. You need to think like the people you are really up against.

No comments:

Post a Comment