Why the Bloomberg rumor came up is unknown as well as their prompt retraction and the disappearance of the retraction posted on Twitter, but I believe this has something to do with an internal struggle at the ECB in which it appears Draghi just lost his majority, which was reflected in late day trade -the last hour and a half or so.

So for all the "Buy the Dip", "The F_E_D has our back", "The ECB will pick up the QE baton", they just suffered a massive moral defeat as those who have voiced opposition to any such plans have outright broken with Draghi, putting him in the minority, if he were ever actually considering QE beyond rhetoric and ambiguous statements he could easily back away from.

In other words, all of the nonsense from the ECB today, looks like it was more of a power struggle that Draghi appears to have lost along with his majority, or because of the loss of his majority as reported this afternoon by Germany's Die Welt:

This is Google Translated so it's not the best, but from Germany's Die Welt, the death of the Draghi majority...

"The outlooks for growth and inflation are bleak. Mario Draghi will therefore open the gmoneyates - and is met with increasing resistance. And on the ECB's Executive Board, he has just lost the majority.

The entire day was all about the ECB, rumors, retractions and truth as well as a last minute surge to keep the SPX green for the week, while the NASDAQ and high Beta Transports are lagging.According to information obtained by "Die Welt", internal resistance to Draghi is now larger than previously thought. He can no longer count on a majority within the Board currently. In the vote on the official opinion of the Governing Council on monetary policy are for information of the "world" three of the six directors supported by the President to the original tune.In addition to Sabine Lautenschlager and Yves Mersch, who had already previously expressed skepticism about bond purchases, one can now add the Frenchman Benoît Coeuré who is against Draghi's course. ...There had been dissenting voices within the Board on several occasions, but there was always a majority behind the President."

Often we see things in 3C, money flows that we don't understand and to wait to understand what they are about is to miss the trade, by the time it's common knowledge the opportunity is long past. As you know we have had a series of macro trends and one of the stranger ones is a strengthening Euro and a weakening dollar, thus perhaps a stronger EUR/USD.

Today with the death of QE or at least no life given to it, the strengthening Euro sent the $USD lower. However, as reported by some as an attempt to ramp the market, the USD/JPY made a trip to new highs above the psychological level of $120 and quickly fell back, as we noted right as it was happening today, THIS WASN'T A LEVER OF MARKET SUPPORT, BUT A LAST CHANCE SHOT AT STOPS ABOVE $120 AND EAST MONEY BEFORE THE WEAK $USD DRAGGED THE USD/JPY OUT OF RANGE OF HITTING THOSE STOPS...PERIOD!

PErhaps between the macro trends of a stronger Euro, weaker $USD with QE now over and a stronger Yen, the days of Central Bank planned economies are coming to a righteous end as Abe may lose his Abenomics mandate in snap elections and Draghi just lost his majority...in that case, the stronger Euro , stronger Yen and weaker $USD on a stronger Euro would all make perfect sense (the macro trends).

As former PIMCO co-counder Bill Gross said today, (paraphrasing), "How can central banks expect to right an economy full of debt by issuing more debt?" Would that work for your household? Of course my opinion which is irrelevant is this has never been about anything other than a stealth banking system bailout as the 2008/2009 bailouts were wildly unpopular with the US voting public, what better way than to use QE which no one outside (and very few inside) the market understand?

While probably not as big of a deal as the developing ECB rift, today did put in the second Hindenburg Omen in 3 days, more on the bearish Hindenburg Omen here for those not familiar... While I'm not a huge believer in it's 100% accuracy, I'll admit we did have a couple right at the September highs that led to the 2-week 1200 point Dow sell-off to the October lows.

As predicted Monday in the Meet Your Levers update, TLT, HYG, USD/JPY, Yields, VXX, VIX and SPY Arbitrage all supported the market Tuesday and Wednesday for the forecasted oversold bounce that we saw coming as early as 10:30 a.m. Monday morning after a parabolic sell-off and large short term capitulation volume-a short term selling climax. And as shown yesterday, Levers Update all were denied to or already failing.

For example, TLT trading up today and Treasury yields on the whole up 1-4 basis points on the day; HYG closing red in to mid-day distribution, VIX accumulation which we covered in detail yesterday via VXX, UVXY and XIV.

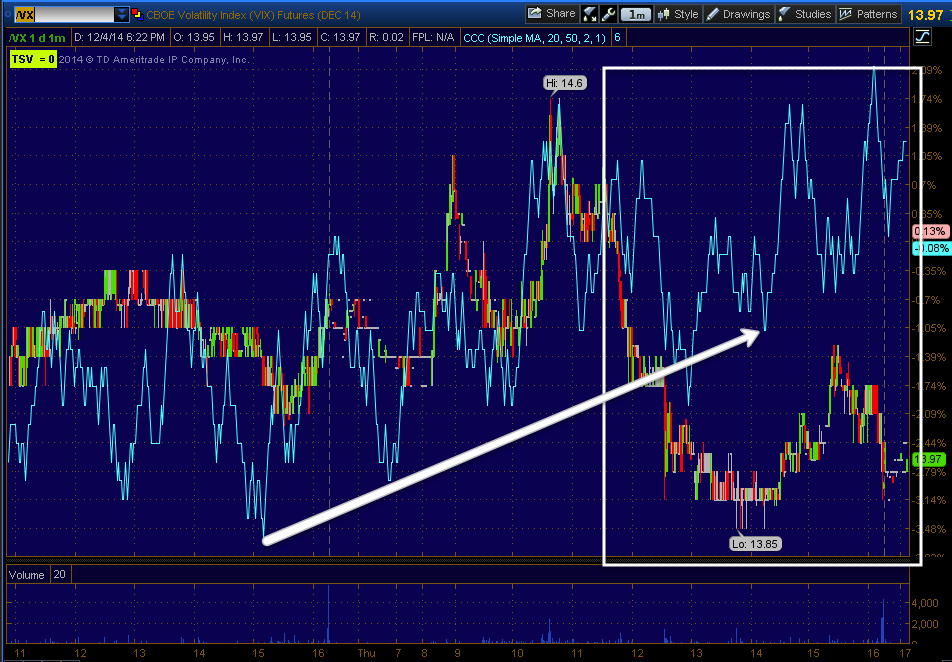

Today VIX futures showed positive divergences in to lows mentioned early in the day, but it just grew from there in to the close.

As seen in Leading Indicators we not only had interesting VIX activity, but HY Credit continues to fail, not a 1-day wonder, but a trend and a fierce one. Pro sentiment continues to fail. Yields reversed and Treasuries were bid in an apparent flight to safety trade, our VIX term Structure indicator that has called nearly every decent bottom with readings at elevated levels above 1 saw the lowest reading in at least a year and a half, in fact going back and looking tonight, today's level of 0.80 was the lowest since 3/15/2013 at 0.79 and while I don't use the indicator for anything other than a buy signal, I counted at least 4 times when readings under 0.85 led to significant pullbacks over the same period mentioned above. Yields were also down today as mentioned (1-4 bps from the short end to the long end), they tend to pull the market toward them just as they did the last 2 days as they rose.

The 10 year closed @ 2.25% and the 30 year at 2.95% today, the worm has turned as yields have been one of my favorite leading indicators next to high yield credit and 3C.

In fact, going in to tomorrow's NFP (8:30 a.m.), I dare say we have not had such large single rally divergences ever since using leading indicators in HY Credit and Yields.

Meanwhile, VIX's range continues to tighten with its Bollinger Bands on a buy signal (only the 3rd signal for this indicator in a year and a half, the other two being dead on...

Given all of the above, I can't understand how anyone aware of the above could possibly sleep at night being long the market when you consider...

Moving along...

Among commodities gold had a slight decline, Silver a gain and copper looks to have had a dead cat bounce, so perhaps there's a copper trade put there as the bounce ends.

As for internals, you already know about the second Hindenburg Omen in 3 days, but that's not anything I consider an edge when the mainstream media is covering it.

As for our internals, There was a Dominant Price / Volume Relationship today unlike yesterday and it was Close Down/Volume Down among the major averages components. The Dow had 14, the NDX with 52, the R2K with 1133 and the SPX with 204.

This relationship of the 4 has the least next day influence, except for this, I call it, "Carry on", in other words, whatever the market was doing, it tends to keep doing it and I wouldn't exactly call today a banner day for the market, but I suspect NFP tomorrow morning will create its own volatility.

Of the 9 S&P sectors, only 2 closed green and they were exceptionally marginal with the leader, Materials at a gain of only 0.30% and the laggard being Energy at a loss of -.87%.

Of the 238 Morningstar groups we rack, a mere 87 of 238 closed green, again very weak performance today.

I'm pretty good at seeing changes in character early, a couple of days ago I mentioned the NYSE % of ALL NYSE Stocks Above Their 200-Day Moving Average (at a mere 50%) was starting to roll over. I've applied a 5-day moving average of the indicator vs the SPX, you can see it is starting to roll over as market breadth which is already in shambles starts to decline again.

Along the same lines near all time SPX highs, the percentage of all NYSE stocks trading above their simple 40-day moving average is at a pitiful 59%, down from the normal 85+% in 2013.

A Quick look at Futures before I end has 3C making new intraday highs in VIX futures, leading positive (See above).

Gold's 5 min 3C futures chart looks like it will see downside in the next day or so as does Silver futures and for now Crude are in line.

Some various Index futures timeframes... (ES=SPX futures / NQ=NASDAQ 100 futures / TF=Russell 2000 Futures)

Es futures (1 min) don't look good, in fact they look to have deteriorated all day.

If I see anything beyond these ugly charts and leading indicators going in to tomorrow morning's Payrolls data, I'll post it as usual.

Have a great night!

No comments:

Post a Comment